Category: Uncategorized

Risk Parity

Risk parity has been one of the most important advancements in portfolio construction over the last decade. It places the focus on equalization of risk and not on comparing expected returns which are notorious for being difficult to forecast. However, there is a problem with risk parity. It will allocate more to low risk asset classes that may be subject to a downturn. There is no opinion on market direction or valuation. It assumes the investor has no information on individual assets or view of factor risks. Outperformance relative to cap weighted portfolio is related to whether low risk assets have returns than higher risk assets.

International Finance

International finance has been increasingly confusing for academics, policy-makers, and traders. Just when you think currency markets will be well-behaved and follow theory, they will move in ways that are totally unexpected. We have always known that currencies are hard to predict given they are expectational markets. Even with perfect foresight about underlying fundamentals, our ability to explain currency is suspect. The research continues to show that currencies are hard to predict and fundamental models can only explain a small percentage of the price variation. There needs to be a deeper framework for understanding foreign exchange behavior.

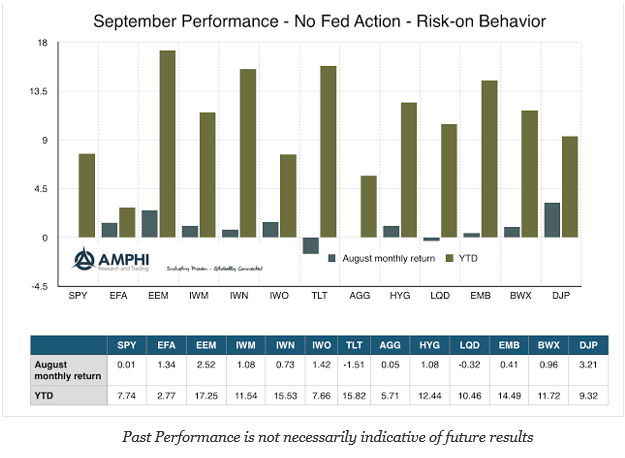

September Performance – Risk-On with Fed on Hold

Was investing for the month so simple? The Fed did not take any action, albeit the threat that they are getting close, and the markets rallied for the month. Fade the Fed regardless of their speeches about wanting to move rates higher. We think this strategy may be ending in December, but right now investors were again rewarded for not believing any threats of Fed action.

Minksy, Volatility, and Skew

The Financial Crisis resurrected the thinking of Hyman Minsky and his “financial instability hypothesis”. With the crisis, there was coined the term Minsky Moment, the time when financial markets collapse after a period of prosperity from the excessive speculation on financial assets. Unfortunately, his insightful views on financial instability never received the attention it deserved before the crisis. It was not structured in the current economic orthodoxy of formal mathematical modeling.

Risk and Return

Risk and return. The drumbeat that return is received in exchange for taking on risk as measured by volatility is relentlessly driven into the minds of all investors, but what if this trade-off is not as strong as the rhetoric? New research focuses on skew as one of the key risks. In particular the downside risk of negative skew may be more important at explaining excess returns than volatility which can lead to either upside or downside.

The Advice of Mr. Jaggers, “Follow the Evidence.”

“Take nothing on its looks; take everything on evidence. There’s no better rule.” — Mr. Jaggers, Pip’s guardian in Great Expectations by Charles Dickens.

If we had Mr. Jaggers as our guardian and mentor, we would likely be better analysts. A recurring theme this month has been about finding the truth through a focus on data, not commentary. Look to the data and not what is being said. If there is no supporting evidence, discount. If no supporting evidence is provided, then find your own. Markets may be driven by sentiment or perception but ultimately it will discount and respond the evidence.

Forgetfulness and Financial Analysis – Is More Memory Always Better?

Big historical events, especially tragedies, are committed to memory so we will not forget, yet is it really good to remember everything? Put differently, is forgetfulness useful? Would we be better off if some memories disappeared?

Financial Analysis and “Truthiness” – Follow Data, Not the Talk

If I were being polite, I would not argue that we are in an age of lies by politicians, businessmen, or leaders, but what The Economist has called a “post-truth world”. Stephen Colbert described the current environment as one of different levels of “truthiness”. At best, clarity by leaders and spokespeople is in short supply. Most commentary is done for spin.

The Paradox of Skill – Why Competitive Markets are Left to Luck

The paradox of skill is an important concept to understand for any investor or trader. Managers will often talk about wanting to prove their skills in a competitive environment against the best in the world. Forget that nonsense. You want to be the best in an uncompetitive or less competitive environment. You want to have a strategy that others do not follow. Being in a competitive space may seem like a good thing, but it will be harder to beat others. If there is a fixed amount of alpha, everyone will be fighting for that same alpha and it will be harder to win your share when the market is more competitive.

Probability of Recession Rising – A Warning

The US recession probability model based on the Treasury spread is a simple straightforward forecasting tool that can be followed in real time. If the spread term negative, watch out, economic winter is coming. Nevertheless, there are only a limited number of recessions and a limited number of signals. What is as useful is watching how the probability of a recession changes during non-recession periods. Periods of growing economic stress will see an increase in recession probability. For example, periods when the probability is more than 10% or even more than 5% will be times when equity markets will be under stress. These periods may pass without a recession, but there will be an impact on financial markets. This signal may have to be confirmed with other data since it provides early warnings, but it is valuable as a simple indicator.

Gemini Alt & IASG Alternatives Announce Technology Integration

CHICAGO, Sept. 13, 2016 /PRNewswire/ — The Gemini Companies announces that its affiliate, Gemini Alternative Funds, LLC (http://www.geminialt.com), has completed a software integration with IASG Alternatives LLC. As part of a strategic relationship, prospective Gemini Alt investors will have access to the IASG Alternatives managed futures database without leaving Gemini Alt’s Galaxy Plus managed account […]

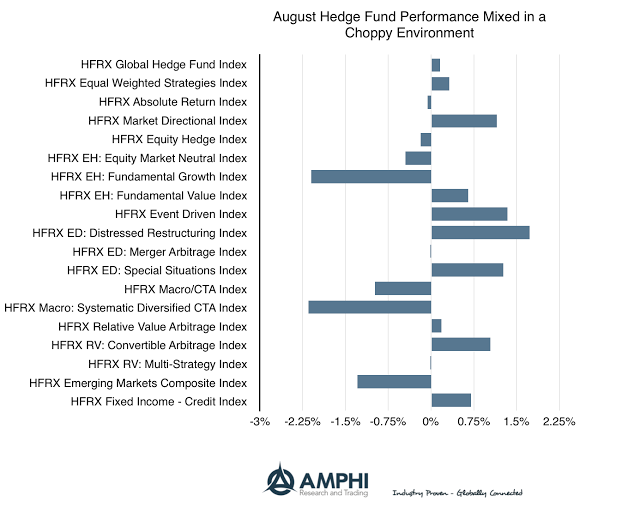

Hedge Funds Performance Shows Dispersion in August and for the Year

2016 is a year is turning out to be special for relative value hedge funds focused on distressed and event driven strategies. These two along with special situations, equity market direction, and convertible arbitrage moved to be the August winner. The losers for the month were fundamental growth and systematic CTA’s. Both these strategies need movement in economic or firm-specific fundamentals which just did not occur for the month. Relative to the flat equity and fixed income markets, August performance for hedge funds was at best fair.

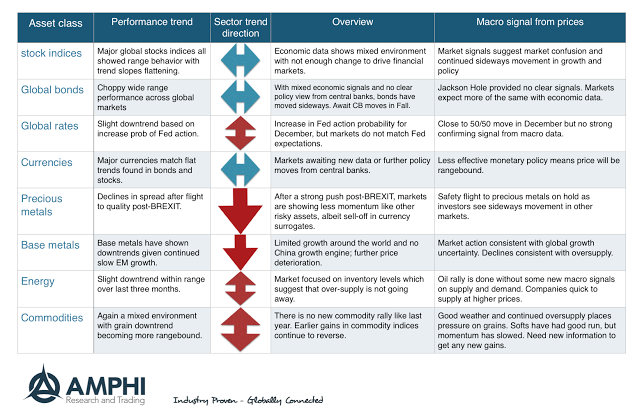

Lack of Trends Across Major Asset Sectors

The reason for the lackluster performance of managed futures is clear from a review of trends for the major sectors. For stock indices, global bonds, and currencies, the big three asset classes, there were no clear trends for the month. Global rates, energy, and commodities also showed sideways movement albeit with a slight downward tilt. The only sectors that showed any real direction were precious and base metals that moved lower.